My cousin got married in May 2016 in Hong Kong.

Robin was 2.5 years old, and Bruce was 10-month-old at the time.

We would have cramped in a less than 800 square foot condo one bathroom with a total of 4 adults and two kids with my family if our entire family went back. So Erwin decided to stay.

My grandma was 84 years old that year.

We weren’t the most resourceful at the time from a financial perspective. It also wasn’t the most convenient time for my kids to go back. They were more than a handful to handle at that age.

I took the kids together with our nanny back home anyway.

That was the last time I saw my grandma in person.

I was planning to spend more time with her this November when our entire family is back for my brother’s wedding. It turns out November was too far away.

It was sudden, she had a stroke and left us within 24 hours.

I’m glad I saw her in 2016, she met my kids but disappointed that I didn’t get to see her again in person.

If there’s one take away, visit the people who you always want to visit before it’s too late, call the friends who you always want to talk to and don’t have the time to do so now.

You may have to go through a lot of trouble, but you’ll be glad you do at the end before you don’t ever get a chance again.

Let’s move onto this week’s topic – maximize the claim on HST you pay when you purchase a vehicle for your business, if this is the case, depending on your location you may want to find the cheapest insurance in NY or see what other states they offer policies to.

If your business is commercial in nature, chances are, you are required to charge HST on your income, AND you are eligible to claim HST you pay on expenses that you incur for earning income.

Simply put, if you earn $10,000 consulting fees, you are required to charge $10,000 plus HST (in Ontario) = $10,000 plus HST $1,300, total of $11,300.

You owe CRA $1,300 – you’re simply collecting on behalf of the CRA.

But you are also eligible to claim the HST you paid on expenses against what you have collected.

If you spend $1,000 on expenses and you paid 13% HST on the expense, you can claim the $130 that you paid against the $1,300 that you collected. Net amount payable to CRA = $1,170.

CRA has a specific term for the HST that you pay on expenses – it is called Input Tax Credit (ITC).

Specific rules applied to different type of expenses, such as meals & entertainment and motor vehicle expenses. Today, we are focusing on passenger vehicles that you use to run your business.

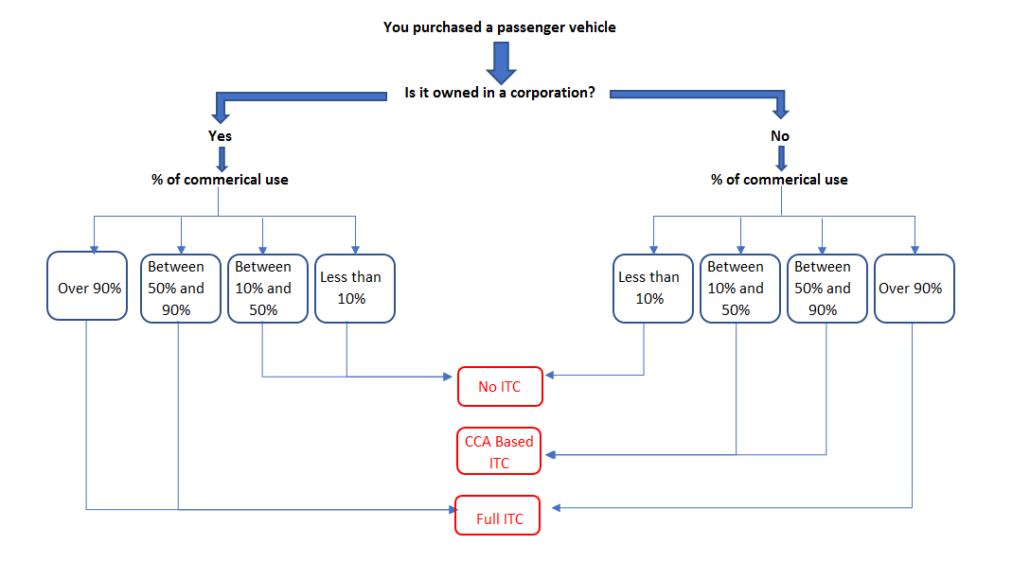

When you purchase a passenger vehicle (I would say the majority of our vehicles are passenger vehicles), you maybe allowed to claim the HST you paid (also known as ITC) on the vehicle against the HST you collected.

The amount of ITC you can claim can be driven by two factors:

- Do you own the vehicle personally? Or in a corporation?

- How much commercial use (meaning that you are using the vehicle to earn the income) do you use?

Since the rules are complicated and difficult to describe, it is easier if I come up with a decision tree for all of you.

What is CCA based ITC?

Say you are self-employed (own your business in your personal name) and you purchase a passenger vehicle during the year for $30K plus HST.

In another word, you pay $3,900 HST on the purchase.

You only use the vehicle 70% for commercial activities use, 30% for personal use.

In this case, you cannot claim $3,900 ITC you paid against the HST you have collected.

Instead, you add this $3,900 ITC you paid to the your “asset” in your tax return.

In other words, you add it to the asset and take a deduction based on business percentage.

Year 1 CCA claimed:

Asset added: $30,000 + 13% HST = $33,900

Maximum CCA allowed = $33,900 x 30% x ½ year rule (for 1st year purchase only) = $5,085

Business use of vehicle = $5,085 x 70% commercial use = $3,360

Year 2 CCA claimed (you can claim 30% of what hasn’t been claimed before)

Maximum CCA allowed = ($33,900 – $5,085) x 30% = $8,645

Business use of vehicle = $8,645 x 70% = $6,051

You are claiming the ITC you paid through depreciation of your vehicle on an annual basis.

If your business use of vehicle increases in a subsequent year, there’s a bigger claim on the ITC you initially paid. If your business use of vehicle decreases, however, a smaller claim is made on the ITC.

What is FULL ITC?

Using the example above, a full ITC claim means that you can deduct $3,900 HST that you pay to acquire the vehicle against the HST you have collected.

Say, during the year, you have charged $100,000 plus HST. You have collected $13,000 HST.

Assuming there’s no other expense, claiming full ITC means that you will remit $13,000 – $3,900 = $9,100 to CRA for your HST liability.

What happens to your vehicle?

Your vehicle is still added as an asset in your tax return whether you are incorporated or not.

Year 1 CCA claimed:

Asset added: $30,000 ($3,900 ITC paid is claimed against income)

Maximum CCA allowed = $30,000 x 30% x ½ year rule (for 1st year purchase only) = $4,500

Business use of vehicle = $4,500 x 70% commercial use = $3,150

Year 2 CCA claimed (you can claim 30% of what hasn’t been claimed before)

Maximum CCA allowed = ($30,000 – $4,500) x 30% = $7,650

Business use of vehicle = $7,650 x 70% = $5,355

There is no relationship between CCA claimed and the HST you pay.

What does NO ITC mean?

No ITC simply means that you cannot claim any ITC against the HST you have collected, and you cannot add the ITC you have paid to the asset pool.

No credit is given if your commercial use is limited.

Rules are complicated around this area of HST. Be sure to speak to your accountant to make sure your claim is correctly calculated.

Until next time, happy Canadian Real Estate Investing.

Cherry Chan, CPA, CA

Yi

What if your vehicle costs more than $30K, and you are a corporation with >90% commerical use, what is the ITC?

Cherry Chan

If your vehicle is more than $30K and it is a passenger vehicle, you can only claim the HST on $30K as ITC.