A bunch of our friends and I started a small charity a few years ago.

Did you know… 37% of Hamilton children go hungry over the holidays.

Our goal was to provide holiday dinners to people who’re in need.

We fed over one thousand families over the last few years.

We started with 37 families in 2014. Real estate investors had started investing even before they could get donation receipts.

We had since become a registered charity, making it official to issue donation receipt to everyone.

Late last year, I saw a Facebook post in a local group asking for a donation of old suitcases. Her family takes a vacation to Jamaica every year in the winter.

She brought school supplies, arts and crafts and toys from Canada to Jamaica. A local cab driver took them to the most underprivileged area, and they hung these small gifts out. The kids were excited.

I didn’t have any suitcases to donate. I offered to buy 10 pairs of shoes.

She was shocked at how excited and grateful the kids were with shoes. Many of them didn’t have proper shoes to begin with.

That got Erwin and I thinking … maybe, just maybe, one dinner each holiday isn’t enough.

Maybe, just maybe, we can provide shoes, jackets and maybe even some toys. Maybe that is a better way to spend our money.

On this Thanksgiving, instead of providing turkey dinners to over 300 families (that’s what we did back in Easter), we decided to do something different. We decided to ask the people what they want.

To our surprise, on top of the shoes and jackets that we expected, they’re asking for groceries, toiletries, underwear, etc.

Things that we totally overlook and take them for granted…

If you want to help, please visit our donation page.

If you want to volunteer, please sign up on the same page.

If you know of shoe suppliers that can donate all the unused shoes, by all means, please connect us.

If you know any corporate donors that are willing to help, email us.

Even a small act of kindness can make a big difference in someone’s world.

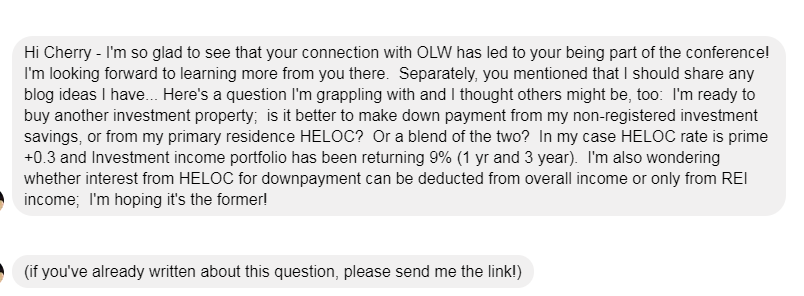

Now onto this week’s topic, I got a client’s question recently and thought I would share here.

She is asking two separate questions here.

- Is it better to invest in real estate using your savings from the non-registered account or use your own primary residence line of credit? Is it better for a blend of two?

- Is the interest deductible from income or is it only deductible from real estate income?

Let’s try to answer the first question here.

Is it better to invest in real estate using your savings from the non-registered account or use your own primary residence line of credit? Is it better for a blend of two?

I’ve got a few people asking me this type of question before. They’re all driven by return on investment, not so much tax impact.

The answer to the question is, it depends.

Prime rate is 3.7% today. HELOC rate is 3.7% + 0.3% = 4%. Cost of investing is 4%.

The decision is often made based on the kind of return you are getting currently from your savings.

If you can earn more than 4% from your investment, you should use your line of credit to buy real estate.

If you earn less than 4% from your investment, you should use your saving as your down payment.

She said that investment income has been returning 9% (1 year and 3 years). I’m not sure what (1 year and 3 year means).

If the investment return is truly 9% annually, I likely will choose to use HELOC for the down payment.

(By the way, I would also like to know how she can do 9% annually. 😉 )

However… you should also consider the following factors:

-

Are you comparing apple to apple?

You mentioned in your message that it was 9% return – but how did you come up with 9%? Just be cautious at how this 9% is calculated. Or whatever this calculation it is.

Sometimes, the 9% is simply pulled out from the investment statement issued by the mutual funds company. Some statements can be quite misleading.

Say downpayment is $100,000, HELOC interest is 4% annually. This is equivalent to $4,000 for the year.

Is your 9% return on investment equal to at least $4,000 cash in the year to cover the cost?

-

What type of return is this 9%? Is it accrued gain on the stock or is it a combination of dividend and appreciation?

Say your investment is also $100,000 and your 9% is purely accrued gain, your portfolio is showing a value of $109K at the end of the year. The market can go up or down the year after. Be cautious with the potential downfall.

Say your investment is producing a 9% dividend yield, you get a cheque for $9K every single year. That’s a true $9K return immediately. That’s more than enough to cover your true cost of $4K interest you incur.

In that case, I would be all for using the line of credit for the down payment of your next investment property.

-

Are you concerned about the cash flow of your property?

If you use your line of credit as the down payment for the property, you would now bear an additional $4,000 of expenses annually.

That’s a whopping $333.33 every month!

This may throw the property analysis out of whack completely.

Are you comfortable bearing this interest cost on a monthly basis?

Most people would rather invest using the cash, knowing for certain that the property is going to make a better return. This goes back to your personal risk tolerance.

This interest expense is certain – the bank will charge you for sure!

Do you gain on investment? Maybe yes? Maybe no?

Do you feel comfortable taking on the risk?

-

Are you planning to buy your next primary residence shortly?

Some investors have zero return on their savings. They keep their cash in the bank.

And it is for this reason that any potential buyer would appreciate it if they know how much they might have to pay at the end of the purchase before they utilize their savings, in which case pages like https://patmcbride.com or others might be of great assistance.

Naturally, when they invest, they want to use their savings first before incurring interest on their line of credit.

However, if you are planning to buy your next primary residence shortly after (and the savings have been used up for your investment) and turn the existing one into a rental, chances are, you’re using your line of credit for the down payment of your next home.

Interest incurred on getting your residence is NOT deductible.

Here, the second question.

Is the interest deductible from income or is it only deductible from real estate income?

Interest expense is deductible from your income. It is not limited to your real estate income.

Some investors, however, choose to track their line of credit interest income against different properties to ensure that they are making a sound investment.

There’s the very small difference between deducting against real estate income and your regular income.

The only difference is the opportunity to take additional capital cost allowance.

Hopefully, it answers your questions.

Until next time, happy Canadian Real Estate Investing.

Cherry Chan, CPA, CA

Your Real Estate Accountant

Marianne

Can you further explain the interest deduction difference if taken against rental income or personal income with capital cost allowance. How does it work and is the difference marginal or significant? Thank you!