One of the most common misconceptions is how we calculate capital gain tax on sales of property.

Many real estate investors would estimate their taxes on a cash flow basis:

Net sales proceeds – mortgage balance

This may be how you calculate how much cash is left in your pocket, but capital gain taxes are not calculated this way fortunately and sometimes unfortunately. 😉

Capital gain is calculated like this:

Capital gain = net sales proceeds – adjusted cost base of your property

If you need a refresher on how capital gain taxes are calculated – here is the link.

Continuing on the same example from the same capital gain tax blog post.

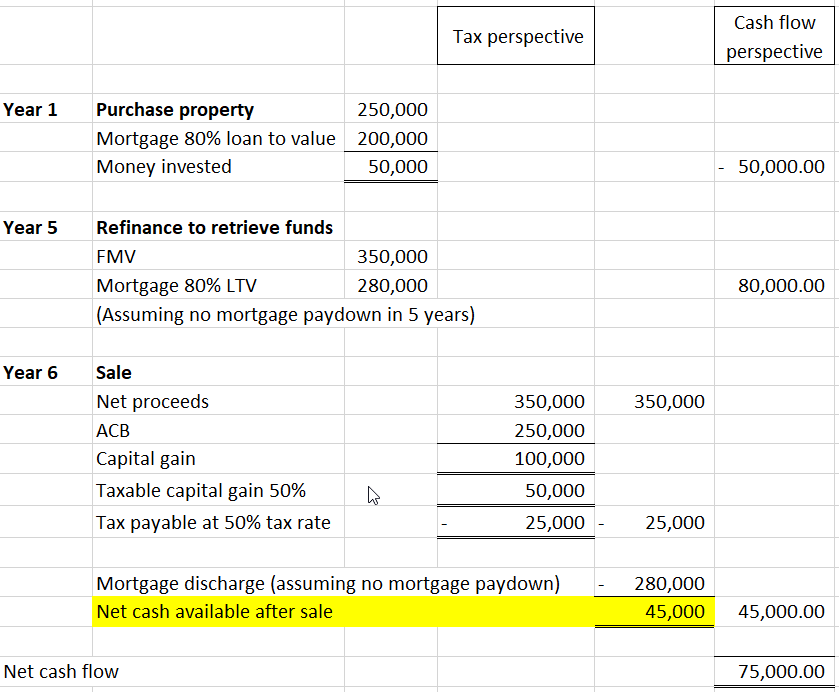

Taxpayer purchased a property for $250K in year 1 with an 80%, interest only mortgage of $200,000. Taxpayer invested a total of $50K.

Taxpayer refinanced the property in year 5 and it was appraised at $350K, got 80% loan to value with a mortgage at $280,000. To keep things simple, it is an interest only mortgage.

Taxpayer sold the property for $350K in year 6.

Myth#1: I sold the property for $350K and my mortgage is $280K. Shouldn’t I just pay taxes on $70K only?

We know from the previous blog post that tax calculation is based on the sale price and adjusted cost base of the property.

Adjusted cost base of your property typically includes purchase cost, land transfer tax, legal fees and all the improvements you’ve made to the properties over the year.

In this particular example, capital gain tax is calculated as below:

Not based on the $70K cash available.

Myth#2: I sold the property for $350K and its adjusted cost base is $250K. I made $100K. Why am I getting less than that from my lawyer?

Well, let’s examine the sequence of events.

Year 1 – the net investment is negative cash flow of $50K.

Year 5 – when the refinance happena, the taxpayer would have gotten $80K out from the refinance.

Year 6 – sale occurred. After paying $25K of taxes, the taxpayer would only pocket $45K.

Combined with the cash flow from all these years – the net after tax profit is $75K.

What if the taxpayer never refinanced?

It turns out, the net after tax profit is the same $75K.

What if the taxpayer refinanced multiple times?

Well, it is possible that you’ve already taken out all the equity from the property. And it is possible that you would end up paying out of your pocket for the taxes on sale.

Make sure you consult with a real estate professional accountant before selling.

Until next time, happy Canadian Real Estate Investing.

Cherry Chan, CPA, CA

Your Real Estate Accountant

Anne Bossy

Dear Cherry, thank-you for the articles on capital gain. My question is, can capitalized improvements be refused at the time of sale? My accountant has put my Keyspire fee as a capital expense, plus we are adding some improvements such as A/C.

Matt C

Hi Cherry, for a Corp, will this capital gain be considered active? Therefore; taxed at 15% instead of 50%?